Teaching Financial Literacy in Middle School: Real-World Money Skills Students Actually Need

Financial literacy is one of the most important real-world topics we can teach middle and high school students. While students learn equations, Algebra, and statistics in math class, they also need opportunities to understand how math affects everyday decisions involving money.

The Texas Essential Knowledge and Skills standards for personal financial literacy, MA.8.12.A–G, focus on helping students become informed consumers, responsible borrowers, and smart savers. These standards connect classroom math to real-life situations students will eventually face—like using credit cards, paying for college, comparing loans, and planning for retirement.

When students see how math applies to real financial choices, engagement increases because the learning suddenly feels meaningful. These are skills that are vital for all middle and high school students including those outside of Texas.

💳 Understanding the Cost of Credit

One of the most eye-opening lessons for students is learning how borrowing money works.

Many teenagers assume that loans simply allow people to buy things they cannot afford right away. What students often do not realize is that borrowing money usually means paying back more than the original amount because of interest.

Under MA.8.12.A, students compare how:

Interest rates

Loan lengths

Monthly payments

affect the total cost of borrowing.

For example, consider two car loans:

Loan A: 3 years at 6% interest

Loan B: 7 years at 5% interest

Even though Loan B may have a lower monthly payment, the borrower could end up paying thousands more over time.

This is a powerful moment for students because they begin to understand that “cheaper per month” does not always mean “less expensive overall.”

Using online loan calculators Loan Calculator — Mr. Slope Guy helps students visualize these differences quickly and makes abstract math feel practical.

📱 Credit Cards and Easy Access Loans

Students are surrounded by advertising that encourages spending now and paying later. Because of this, MA.8.12.B is especially important.

This standard asks students to calculate the total cost of repaying loans under different interest rates and time periods. Students also explore:

Credit cards

Payday loans

Easy access loans

Installment plans

Many students are shocked to discover how quickly debt grows when only minimum payments are made.

For example:

A $1,000 credit card balance

At a high interest rate

With minimum payments only

can take years to repay.

Students quickly learn an important financial lesson:

Borrowing money can make purchases more expensive than expected.

Activities involving online calculators allow students to experiment with different interest rates and repayment periods. This hands-on exploration builds critical thinking and problem-solving skills while reinforcing percent and decimal concepts.

🌱 The Power of Saving Small Amounts

One of the best financial habits students can develop is consistent saving.

Under MA.8.12.C, students learn how small amounts of money invested regularly can grow over time.

This is where students begin to see the magic of long-term investing.

Imagine saving:

$10 per week

$25 per month

or part of a birthday gift each year

At first, the amounts seem small. But over time, savings can grow significantly through interest and investment growth.

Students often believe that investing is only for wealthy adults. Teaching this standard helps them realize:

Anyone can start saving

Small habits matter

Time is one of the greatest financial advantages

This lesson also introduces students to saving for:

College

Emergencies

Retirement

Future goals

The earlier students understand this concept, the more likely they are to develop healthy financial habits.

📈 Simple Interest vs. Compound Interest

One of the most valuable financial literacy lessons students can learn involves comparing simple interest and compound interest.

Under MA.8.12.D, students calculate and compare these two types of earnings.

Simple interest is calculated only on the original amount.

Compound interest, however, earns interest on:

the original amount

plus previously earned interest

This creates long-term growth.

A helpful example is:

Student A saves $1,000 using simple interest

Student B saves $1,000 using compound interest

Over time, Student B’s money grows faster because the interest continues building upon itself.

Many students find this concept fascinating because they begin to understand why adults talk so much about investing early.

This lesson naturally connects math skills with future financial planning.

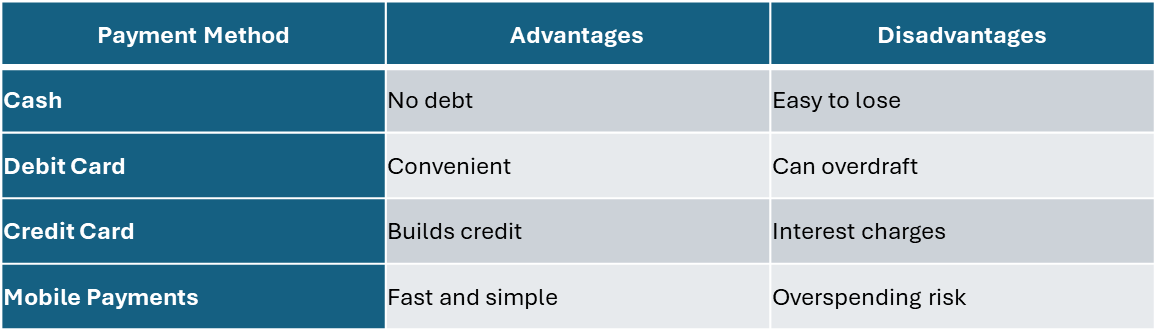

💵 Comparing Different Payment Methods

Today’s students see many ways to pay for purchases:

Cash

Debit cards

Credit cards

Mobile payment apps

Buy-now-pay-later services

Under MA.8.12.E, students examine the advantages and disadvantages of each payment method.

For example:

This standard encourages students to think critically about convenience versus responsibility.

Many middle school students already use digital payment systems through family accounts, gaming purchases, or online shopping. These conversations feel highly relevant to them.

✅ Financial Responsibility vs. Financial Irresponsibility

One of the most important life lessons in financial literacy is understanding consequences.

Under MA.8.12.F, students analyze whether decisions represent responsible or irresponsible financial behavior.

Examples of responsible decisions:

Saving before making a purchase

Comparing prices

Avoiding unnecessary debt

Creating a budget

Examples of irresponsible decisions:

Overspending

Ignoring bills

Using credit carelessly

Making impulse purchases

Students begin to understand that financial decisions today can affect opportunities tomorrow.

This standard promotes decision-making skills that extend far beyond math class.

🎓 Planning for College Costs

College can be expensive, and many students have no idea how much it actually costs.

Under MA.8.12.G, students estimate:

Two-year college costs

Four-year university costs

Family contributions

Savings plans

Students also create periodic savings plans to help contribute toward future college expenses.

This is one of the most practical and empowering standards because it helps students realize:

College costs can be planned for

Scholarships and savings matter

Starting early helps tremendously

Students can compare:

Community college tuition

Public university costs

Housing expenses

Meal plans

Transportation

Books and fees

From there, students calculate how much money would need to be saved monthly or yearly to help cover expenses.

This lesson transforms financial literacy into future planning.

🚀 Why Financial Literacy Matters

Financial literacy gives students tools they will use for the rest of their lives.

When students understand:

interest,

loans,

saving,

investing,

budgeting,

and responsible spending,

they are better prepared to make smart financial choices as adults.

These TEKS standards help students move beyond simply solving math problems. They help students become thoughtful consumers, informed borrowers, and confident planners for the future.

And perhaps most importantly, financial literacy helps students realize that small financial decisions made today can create big opportunities tomorrow.

📚 Looking for Ready-to-Use Financial Literacy Activities?

If you’re teaching TEKS-aligned personal financial literacy skills in middle school, having engaging and meaningful resources can make all the difference.

This comprehensive bundle covers essential real-world topics including:

Loans and interest

Budgeting

Credit cards

College costs

Saving and investing

Financial responsibility

Personal Economics and life skills

Perfect for:

8th and 9th grade math

Financial literacy electives

Homeschool

Reading Comprehension

Advisory classes

Career readiness

Sub plans

Independent practice

👉 Check out the resource here:

Financial Literacy Activities Bundle Grades 8 and 9 for Life Skills & Economics

Designed to help students connect classroom math to real-life money decisions, this bundle makes financial literacy practical, engaging, and easy to teach.